3 Tax Things To Consider For Your Investment Portfolio

Somewhere between a root canal and a trip to Hawaii lies doing our taxes. However, I find this to be an opportune time to reflect across all your financials.

Somewhere between a root canal and a trip to Hawaii lies doing our taxes. However, I find this to be an opportune time to reflect across all your financials.

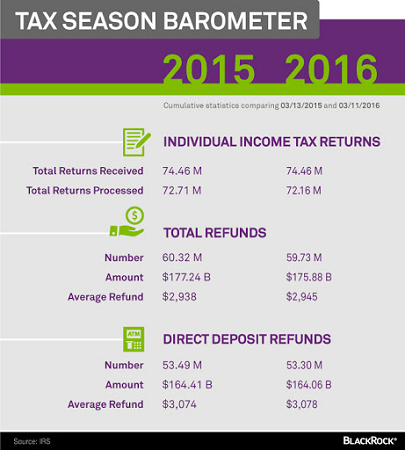

As of March 11 this income tax season, the IRS has already received over 74 million returns and doled out approximately $176 billion in tax refunds.

If you’re in this camp, good for you! For the rest of us, we’re knee-deep in gathering paperwork and filling out those tax forms. Schedule Ds, 5498s, 1099-DIVs, 1099-Rs — clearly, your taxes and investments are related.

It is worth a pause amid the frenetic tax season to remind ourselves of the connection between our taxes and our investments; and savvy investors pay attention to both.

To get you started, here are three connection points and actions to consider for tax season. First and most basic — contribute toward your future; second is to use potentially tax-friendly investments such as ETFs; and lastly, make sure that tax return doesn’t sit in cash for too long.

1. Contribute to your retirement accounts. Did you know that this year you can contribute to your IRA until April 18 for it to count toward 2015 deductions? The traditional Tax Day of April 15 is Emancipation Day, a holiday in the District of Columbia, so you get another full weekend to prepare and boost your traditional or ROTH IRA (be sure not to exceed the annual contribution limit).

Depending on your income, however, you may not be able to deduct IRA contributions if you also have a 401(k) at work. If so, set yourself up for 2016 and beyond by making sure you are contributing as much as you can toward your 401(k), up to the allowable limit. This not only lowers the amount of income tax deducted from each paycheck you earn now, it also maximizes any potential employer match. These tax-friendly actions can help you reduce the risk of not having enough retirement savings when you need it.

2. Look for tax-efficient investments. Many people don’t realize that the taxes you pay on the capital gains associated with trading inside an investment fund are costs that affect your total return, if you’re not invested in a tax-deferred retirement account. Consider switching some of your investments to exchange traded funds (ETFs). Because of their structure, ETFs typically pay out less in taxable capital gains than mutual funds. In fact, Morningstar data as of the end of 2015 indicates that only 7% of iShares ETFs paid capital gains distributions in 2015, compared to 58% of mutual funds.

3. Invest that refund. The average refund has been about $3,000. Certainly, there are many things you may want or need to do with that money, such as pay off expensive debt. But if you can, consider investing it in low-cost ETFs that serve the core of your portfolio and allows that money to work for you over time. If you’re saving for a short-term goal (over 6 months), a bond ETF may provide a better return for a little more risk than a bank savings or money market account.

And if you’re not expecting a refund this year, refer back to steps 1 and 2 for tax year 2016.

Sometimes the tax-man giveth

By taking just a bit of time to follow a few simple steps, tax season can be an opportunity to help prepare your assets to grow, and grow some more over time. While the tasks may never feel the same as a trip to Hawaii, being tax efficient could potentially add to your “Save-for-Vacation” fund. Aloha.

Note: Heather Pelant is the author of this article and is a contributor to EconMatters.com.

Category: Investing in Penny Stocks