Universal Personal Finance Rules

Ever heard of the saying, the more we’re different, the more we’re the same. This applies to our personal finance situation too.

Ever heard of the saying, the more we’re different, the more we’re the same. This applies to our personal finance situation too.

All of us want to feel financially secure.

If we have kids, all of us want to provide for our kids.

All of us are willing to take a certain amount of risk, whether that is super-small (i.e. a money market account or super big – a venture fund).

So what are some of the personal finance rules that are universal?

Rule Number 1: Save Invest More Than You Earn

This is probably the most basic and fundamental rule in personal finance. You can’t invest if you don’t save. And you can’t save if you spend more than what you earn. But I’ve put a bit of a twist on the rule and instead of saying “save more than you earn”, I’m saying “invest more than you earn”.

Saving and investing are clearly different. Saving just means to take some of your money and put it in a bank account, where it hardly works for you. While investing is taking some of your money and making it work hard for you; very different concepts.

There are percentages all over the internet that will recommend how much of your income you should be investing every month. If you’re just starting out, I would recommend taking baby steps in your investing plan so the task is not overwhelming. For example, if you’re earning a net of $1,000 per month, try to invest 10% of that – $100.

You’ll learn to live your life off of $900 per month and the future you will thank you. And then a few months down the line try to increase it a little bit more.

Maybe you can learn from budgeting your expenses how to optimize your financial life to invest more.

Finally, when you receive a raise or promotion, take as much of that as you can and dump it into your investments.

Rule Number 2: Diversify Your Investments

We all may have different investment strategies. For the past couple of years, I’ve been gravitating more towards a passive approach of buying into ETFs and Index Funds.

But I know there are investors out there who prefer a more active approach, which is buying single stocks.

Both investment methods will improve your personal finances. I prefer the passive approach of ETFs and Index Funds because there is overall less reading, research and maintenance involved.

Even though there are two approaches here, all of us can agree that both strategies of investment require diversification – having multiple investments across various sized companies and sectors.

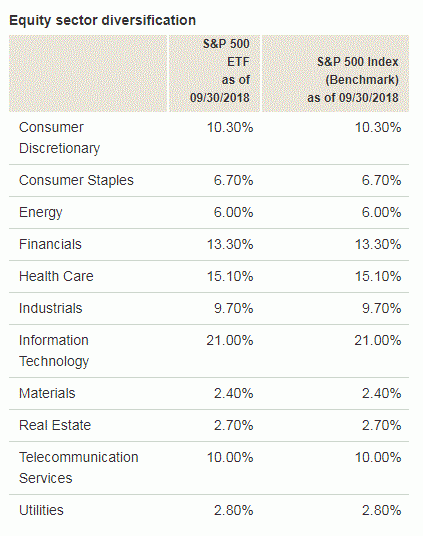

With ETFs and Index Funds, this is easy as they allow you to automatically diversity when you buy into a specific fund. For example, the Vanguard S&P 500 ETF, VOO consists of 509 stocks. And in terms of diversification, here is the breakdown from Vanguard’s website:

With individual stocks, you have to make sure your portfolio or basket of stocks include various sectors such as financial services, healthcare, technology, utilities, etc.

Personally, I’d recommend an individual stock investment method to investors who have more time, a greater interest in personal finance and investing and the ability to continually monitor and track the performance of their investments and make adjustments accordingly.

When I was single and without kids, my portfolio was heavier with individual stocks and most of the time, they performed well. Now, being married and with two little kids, I decided that the passive approach of fund investment allows me to free up more time to devote to family.

Rule Number 3: Follow/Monitor You Savings and Investment Rules

You know that clever thing that people do when they bring up rule number 2 and it’s usually something like don’t forget rule number 1. Well, this is kind of like that.

In order for us to achieve our financial goals, we need to be continuously following our rules. That means we need to develop habits.

A popular figure on the web is James Clear. I’ve heard a lot of good things about a book he has written entitled Atomic Habits. Although I haven’t read the book myself, I understand and wholeheartedly agree that in order to adopt good habits; you need to create an environment where they can be adapted easily.

For example, if you want to save consistently, establish an environment that will allow you to do so easily. This can mean working with your payroll department so a portion of your paycheck can automatically go into your savings account rather than your checking account. You may feel it in the first few pay periods, but over time you will learn to live with less and the funds in your savings will accumulate. Then you’ll be able to invest those into a diversified investment strategy from Rule Number 1.

Following also means monitoring. As your investments start to gain value, it’s a good idea to revisit them. Why is it a good idea? If they are gaining in value, why would you ever want to disturb that? That’s a good point and the reason is to reduce risk and over-exposure to one or more sectors and continue to maintain diversification.

For example, if your investment plans, which is designed for your personal financial goals calls for international stocks to be at 20% and they are now 30% of your portfolio due to gains in the international market, you may want to rebalance your portfolio to (1) sell off some international stock and lock in these gains, and (2) reduce the risk of the international stocks falling within your portfolio, and (3) continue to maintain diversification in your portfolio in alignment with your personal financial goals.

Note: This article originally appeared at Simple Money Man.

Category: Personal Finance