Train Your Brain – Red Is Good, Green Is Bad

We’ve all heard the timeless advice from Mr. Warren Buffet, buy low and sell high. But do we really follow it much? It’s definitely easier said than done. Have we trained ourselves to think and act like Mr. Buffet?

We’ve all heard the timeless advice from Mr. Warren Buffet, buy low and sell high. But do we really follow it much? It’s definitely easier said than done. Have we trained ourselves to think and act like Mr. Buffet?

When the market is dropping, we may feel like selling our investments thinking to ourselves, hey let me cash in now before it drops even more and I lose even more money than I already have.

The problem is that we let our emotions take over and as a result have sold at a loss. The fact that the market as a whole dropped may have nothing to do with your investment’s performance on that particular day or even week.

How can we avoid this emotional roller-coaster? Well, one strategy I’ve been working on internally is to train my brain. I’m deliberately making myself believe that when the market has dropped, it’s good and when the market rises, it’s bad.

Works For Long-Term Investors

Many years ago I decided to change up my investment strategy from essentially flipping stocks to buying and holding of the long-term.

Generally, when you’re a long-term investor, you’re buying more and selling less. You really only sell positions to rebalance your portfolio; that is sell winners.

Of course, my work retirement account will continue to engage in dollar-cost averaging into index funds. So at times it will buy high and other times low. However, there will be consistency and the costs will be spread out.

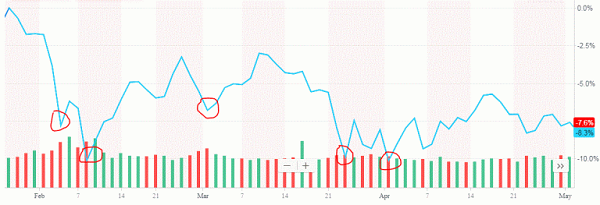

I was kicking myself a bit this past February. The S&P 500 had dropped over 10% and I wasn’t in a position to buy because I didn’t employ my train your brain philosophy.

The market peaked towards the end of January. Since then, it has dipped about 5 times – all buying opportunities:

The Past Is The Past

As I mentioned before, In my earlier investing days, I made hasty decisions based off of market behavior. Of course, I suffered and in those days. First, I sold at a loss and had lesser funds to reinvest into something else. Also, just weeks later the investment I sold at a loss recovered and nicely surpassing my original costs basis.

The only silver lining was that I could claim some of the loss on my taxes. And I’m thankful that I made those mistakes early on. Still, though, there is no guarantee that I won’t make some other mistakes either.

Long-Term Advantages And Goal Alignment

The long-term strategy is favorable for many reasons. Some of the reasons why long-term investing is favorable include:

- it doesn’t involve constant research and market tracking,

- less stressful during times of volatility,

- less money to be paid in commissions,

- capital gains tax rates are a lot lower. Short-term trading results in tax rates of up to 39.5%, whereas long-term capital gains taxes peak at 20% – a difference of almost half. After all, doesn’t it really come down to how much you get to keep in your pocket?

Apart from interest and dividend payments, you’re actually really making money when you realize your investments by selling them.

Since I have many years until retirement, my goal is to buy, not sell. And buying at discounted prices is always a plus. Therefore, I’ve trained my brain into thinking that when the market falls, it’s good, when the market rises, it’s bad.

You’ll Know When The Market Is Red

If you follow the market on a regular basis, you’ll know when it’s dropped significantly, thus representing an opportunity to buy.

Another way to ensure you buy low is to set-up a limit order with your broker. When the price of an investment drops by a given percentage let’s say 5% or more, then the order will be executed.

In order to be prepared, make sure you have some funds in your brokerage or IRA account to strike while the iron is hot.

My Modified Lump-Sum Approach

I’ve recently read that it’s better to invest a lump-sum of money rather than chunks at a time.

While this may be true, I’m not fully comfortable deploying a large sum all at once. At the same time, I don’t want to be at a disadvantage either by not adhering to this philosophy and missing out on gains.

So I’ve adopted a modified approach where I plan to deploy a sizeable chunk each time the S&P index funds I like drops by 3% or more within the course of a year. If I have any funds left after the year is over, they will be invested as a lump-sum. Hopefully, this will allow me to continuously invest and not be impacted as much by major losses.

It’s Different For Retirees

The train your brain philosophy is ideally suited for long-term investors who have 10 plus years until they decide to retire. Understandably when you’re retired, your main source of income may only be the withdrawals from the nest egg you’ve built up.

Nevertheless, when the market drops significantly, your account shouldn’t. Your retirement account shouldn’t be significantly affected because it should consist of assets that are a lot less volatile (e.g., bonds and other fixed-income instruments). At this point, you’re probably not buying anything, but instead making distributions.

Don’t associate with red in the market with fear and anxiety. Train your brain into welcoming and embracing the chaos. It may take time for our whole investment life we get excited when the market skyrockets.

Just think to yourself that hey since I am long-term investor I buy a lot more and sell a lot less. And because of that exact reason, red is good and green is bad.

Note: This article originally appeared at Simple Money Man.

Category: Personal Finance