Earnings Could Be Stronger Than Ever; Growth And Small-Caps Time To Shine?

Key Takeaways

Key Takeaways

- We forecast 8–10% returns for the S&P 500 in 2018.

- The S&P 500 is well positioned to generate strong earnings, in our view, thanks to better global growth and potentially lower corporate tax rates.

Back to business: fundamentals to drive stock market gains in 2018. With a focus on business fundamentals and the impact of fiscal policy, the return of the business cycle means that earnings growth may have to shoulder most, if not all, of the load if stocks are going to produce attractive returns in 2018.

The good news is the S&P 500 Index may be well positioned to generate earnings growth at or near double-digits in 2018 thanks to a combination of better economic growth and potentially lower corporate tax rates, despite some possible downward pressure on profit margins from higher wages.

We also expect the stock market’s price-to-earnings (PE) multiple, at 19.5 times trailing earnings, to hold steady (or drop slightly) in 2018, as the economic cycle ages, inflation picks up modestly, and central bank policy tightens further*.

Risks to our stock market forecast include Congress failing to pass a tax agreement (a low risk after Senate passage over the weekend), a potential policy mistake by a central bank, and political uncertainty around the midterm elections.

*The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with a lower PE ratio.

Earnings Could Be Stronger Than Ever

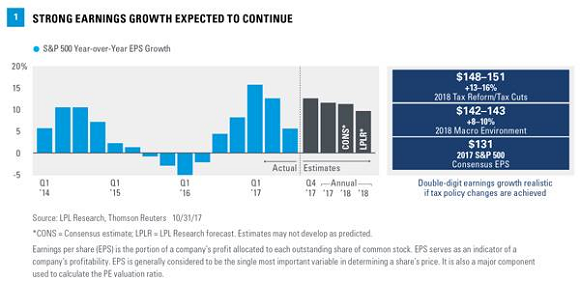

After three straight years (2014–2016) of basically flat S&P 500 operating earnings, at around $118 per share, consensus estimates project $131 earnings per share (EPS) for 2017 and $146 per share for 2018. Earnings are supported by better global economic growth, including a pickup in business spending and robust manufacturing activity, normalized inflation (near 2%), and stable operating margins, even with some modest wage and other input cost pressures.

Should tax reform, or even just a lowered corporate tax rate, be achieved, earnings may get another 5–6% boost on top of that, putting numbers above the consensus $146 per share potentially in play. To break that down, a favorable macroeconomic backdrop supports mid- to high-single-digit earnings gains in the next year, consistent with long-term trends, resulting in our forecast of 8–10% growth, or roughly $142–143 for S&P 500 EPS for 2018 [Figure 1]. Our forecast does not include any direct impact from the tax bill because passage is not assured at this time (although likely) and final details remain unclear. We would identify earnings growth in the 13–16% range as the upside potential we may see from tax reform.

Some Other Leaders To Turn To

A focus on business fundamentals and the impact of fiscal policy will have implications for equity leadership across size, style, sectors, and geography.

Small Cap Opportunity

Since the initial post-election rally late in 2016, small caps have had a difficult time keeping up with the strong performance of large caps, at least until September 2017 when prospects for tax reform began to improve. Small caps generally pay higher tax rates than large caps—we estimate 5% higher on average—so any potential tax reform would benefit this group significantly [Figure 2].

As the monetary policy ball is handed off to fiscal policy and a more typical business cycle emerges, small cap performance may improve. That hinges on the White House and Republicans reaching a tax deal that can get passed through Congress. Small cap, which are more domestically oriented companies, are also in a better position to weather a potentially stronger dollar due to their higher proportion of domestic revenue.

Technicals are also supportive of small cap. The trend for small cap performance relative to large caps is favorable, suggesting small caps may be poised to outperform large caps in 2018.

We see the risk to small caps related to the age of the business cycle as manageable at this stage, but small caps may underperform should a potential stock market correction materialize. It is also important to keep in mind, the prices of small cap stocks are generally more volatile than large cap stocks.

Style

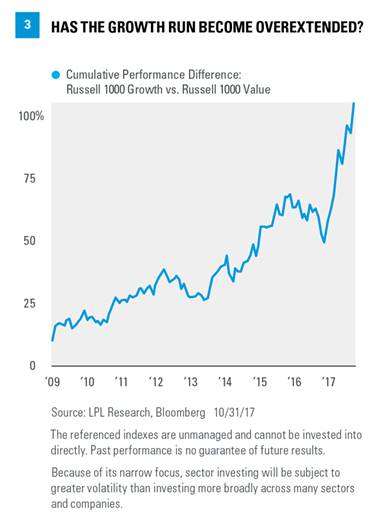

Growth has been on a roll, outperforming value significantly so far in 2017. That leadership is nothing new, as growth has outpaced value consistently for a decade in what has been one of the longest periods of growth outperformance in history [Figure 3].

As markets return to more traditional business cycle drivers, several dynamics may contribute to a better environment for value stocks. The value style tends to perform better when economic growth accelerates, which we expect to see in 2018, especially if fiscal stimulus is put in place and corporate tax rates are lowered. The gradual acceleration since the first quarter of 2017 has not benefited value, suggesting that benefit could still be forthcoming. Higher interest rates as growth and inflation pick up, and a potentially steeper yield curve, may also support better value performance in traditional value plays such as financials; while strength in technology, the biggest growth sector, may moderate even if the sector outperforms as

we expect.

Sectors

We expect cyclical sectors to outperform their defensive counterparts as the economic expansion continues. Our favored sectors include:

- Financials. May benefit from an acceleration in loan growth, deregulation, and a steeper yield curve as monetary policy stimulus is removed.

- Industrials. May benefit from stronger global economic growth, a pickup in business spending, and increasing government defense budgets.

- Technology. May benefit from a pickup in business spending, product innovation, and the sector’s role as a productivity enabler.

Because of their narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

Regions

From a regional perspective, we favor the U.S. and emerging markets (EM) over developed foreign markets broadly, although the improving outlook in Japan is noteworthy. When looking at a combination of economic growth (favors U.S. and EM), earnings growth (favors U.S. and EM), relative political stability (favors U.S., Japan, and China over Europe), and valuations (favors EM), we see the U.S. and EM having the most favorable risk-reward profiles.

When possible, we suggest hedging currency exposure in developed markets, which would make these markets more attractive to us given our expectation that the U.S. dollar will rise

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Note: This article was contributed to ValueWalk.com by LPL Financial.

Category: Small-Cap Stocks