What Exactly Is Credit?

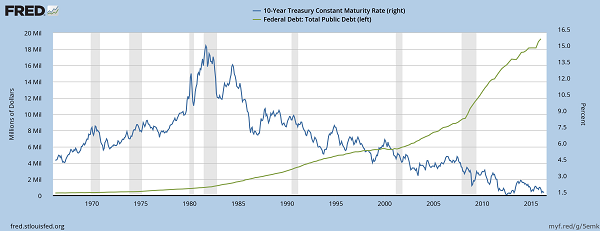

Today, the yield on the 10-year treasury hit a record low of 1.378%. Given that data for this security go back to 1790, – a 226 year span that includes Civil War, two world wars, and multiples periods of economic upheaval, – this development is interesting, to say the least.

Today, the yield on the 10-year treasury hit a record low of 1.378%. Given that data for this security go back to 1790, – a 226 year span that includes Civil War, two world wars, and multiples periods of economic upheaval, – this development is interesting, to say the least.

What’s more, the price of debt (remember, prices move inversely to yields) have climbed inexorably even as supply (national debt) has increased dramatically. That price and supply should increase simultaneously would be considered an economic impossibility by many economic models:

I am sure that there will be many explanations for the dramatic fall in yields despite the huge new supply of government debt. The usual suspects will trot out the tired arguments that years of ZIRP (zero interest rate policy) and trillions in quantitative easing (“QE,” or the Federal Reserve’s bond buying program) have conditioned the markets to expect that any softness in the economy either domestically or abroad will be met with further stimulus from the central bank.

Readers of this blog will note that while these theories are convenient, – after all, there is a strong tendency for people to equate correlation with causation, – they are also incorrect, primarily because they lack a fundamental understanding of what exactly credit is.

A study of the word itself is revealing. The word credit derives from the Latin word ‘credere,’ which means to believe or trust. To have credit with someone means that that person believes in you. In financial terms, if you have good credit, then others are more likely to put their money in your hands as they believe in your future prospects. Simply put, they feel fairly confident that they will get their capital returned to them on time and intact.

The main reason investors are willing to buy treasuries hand over fist and finance Uncle Sam’s burgeoning deficits is because the United States Treasury has enormous credit with investors, the legacy of never having defaulted on its obligations (except for a minor technicality), and having the largest and most dynamic economy in the world. This is in stark contrast countries like Honduras and Nicaragua that have little to no debt, primarily because they do not have credit with lenders.

But any discussion of credit and what it is should not be relegated simply to the world of sovereign debt. As Mr. Tamny’s new book, Who Needs the Fed, puts it, credit is not something that can be decreed; it is something that is earned, and that can be lost.

Consider the case of a young man just out of college, and interviewing for his first job. He has credit with his would-be employer based on his resume of past achievements, both academic and professional, and so the employer is willing to invest time and money in this new hire. As Tamny explains, whether the Fed is easy or not at this point is immaterial to this basic economic transaction. All that matters is whether the candidate has sufficient credit with the employer to win his confidence.

This concept of credit is illustrated very well by the saga of the PIMCO Total Return Fund (PTTAX). which was once the world’s largest mutual fund. When times were good and the fund performed, investors piled into the fund in droves. However, as performance lagged and the fund’s star manager, Bill Gross, departed, investors have exited in great numbers. As a recent Wall Street Journal article noted, “PIMCO Total Return has bled assets every month since May 2013, slimming to its current $86.1 billion from $292.6 billion at the end of April 2013…” Clearly, whether through poor performance or management instability, or perhaps a combination of the two, the fund has lost credibility with a majority of its investors, the net result of which is asset attrition to the tune of -70%. It goes without saying that this has occurred during a period of relatively accommodative Fed policy, not much of which added to the creditworthiness of PIMCO’s star bond fund.

In sum, until we have a better understanding of what exactly credit is, we will continue to make the mistake of believing that government and central bank policies have more of an impact than they actually do, and we run the risk of misallocating capital based on this belief. We cannot fault policymakers for doing what they think necessary to stimulate moribund economies, but a simple glance at the evidence reveals that despite their best efforts, no amount of policy action will ever take the place of economic dynamism, creative destruction, and the perpetual quest of capital to end up in the hands of those who will use it most wisely.

The information provided above is obtained from publicly available sources and it is believed to be reliable. However, no representation or warranty is made as to its accuracy or completeness.

Note: The author of this article is Lawrence Hamtil and he is a contributor to ValueWalk.com. Click here to visit the site directly.

Category: Breaking News