A Small-Cap Pause That Refreshes?

Co-CIO Francis Gannon analyzes the cross-currents and reversals in 1Q17 and details why the small-cap rally has room to run.

Co-CIO Francis Gannon analyzes the cross-currents and reversals in 1Q17 and details why the small-cap rally has room to run.

Observations on a Curious Quarter

2016’s Reversals Reversed

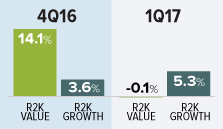

Stocks saw reversals in leadership based on market capitalization, style, and sector in 1Q17. Large-caps outpaced small-caps, growth beat value, and healthcare stocks shook off a weak 2016. In fact, what worked best in 2016, especially in the fourth quarter, did not work in 1Q17—and vice versa.

For the quarter, the Russell 2000 Index was up 2.5%. The Nasdaq led the domestic indexes, up 9.8% in 1Q17, while the large-cap Russell 1000 (+6.0%) and S&P 500 (+6.1%) Indexes were also solidly positive. The Russell 2000 Value Index slipped just slightly, down 0.1% for 1Q17 versus a 5.3% gain for the Russell 2000 Growth.

At the sector level, Health Care rebounded from its 2016 doldrums to lead the Russell 2000 while Energy—one of the stronger areas for the Russell 2000 in 2016—fell farthest for the quarter. (The index’s remaining nine sectors had more mixed results for the quarter.)

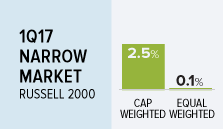

Small-Cap Leadership Was Narrow

Small-cap leadership was narrow in 1Q17, the 2.5% capitalization-weighted gain for the Russell 2000 was markedly better than its 0.1% gain on an equal-weighted basis.

To be sure, this is common in growth-led rallies and suggests that the market was weaker than it appeared, an observation borne out by the fact that healthcare’s leadership was itself confined primarily to the sector’s biotechnology, pharmaceutical, and healthcare technology industries.

We certainly did not see a broad-based move for growth as a whole in 1Q17.

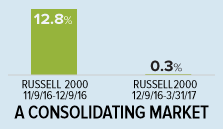

The Market Is Consolidating

With 2016’s laggards catching up and some of last year’s stalwarts falling behind or treading water, it looked to us like the market was consolidating, working to digest the lofty gains from the previous several months. The Russell 2000 was essentially flat, as well as fairly range bound, from its 2016 high on 12/9 through 3/31/17, gaining only 0.3% over the period.

Entering March, a consensus emerged that expectations for 2017 may be too high, a view arguably reinforced by concerns that the timeline for new stimulative fiscal policies may extend into 2018, tempering the postelection optimism that animated 4Q16’s market.

The current small-cap cycle seems to be experiencing a correction in time, in which future earnings need to catch up to current prices.

Looking Beyond the Quarter

The Resilient Small-Cap Cycle1 Has Room to Run

We expect small-caps to resume their advance later this year. The tension between the view that current valuations are too high and the idea that economic acceleration will fuel equity prices suggests to us that stocks are in fundamentally sound condition, in spite of valuations that looked admittedly rich for the market as a whole at the end of March, being based on more realistic expectations.

We’re also very encouraged by the resilience of the current small-cap rally. In the span of less than a year, markets have been rocked by Brexit, the highly contentious election, and the false start on healthcare reform.

Yet none of these events has done more than temporarily slow the overall upward move for small-caps—led for the cycle by value and cyclicals.

This cycle began with the small-cap trough on 2/11/16. So we think it’s important to remember that it is both much younger than the current large-cap cycle, which dates back to the post-Financial Crisis trough on 3/9/09, but also did not first materialize after the November elections.

Our own focus is on our analysis of, and communication with, individual companies, so we see the rally as having a more substantial foundation. We are therefore not as concerned as some investors are with developments in Washington.

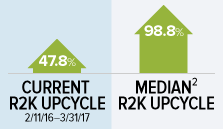

We think it’s also important to recall the history of small-cap rebounds. There have been 12 declines of 15% or more since the Russell 2000’s inception in 1979. The median return in the subsequent recovery was 98.8%. From the Russell 2000’s trough on 2/11/16-3/31/17, the small-cap index rose 47.8%.

History suggests, then, that we are less than halfway through—making the cycle young not just in terms of time, and with more to come.

1At Royce, we define market cycles as periods that have declined at least 15% from a previous market peak and then rebounded to establish a new peak above the previous one. Each must comprise a peak-to-trough and trough-to-peak period.

2Median includes only full recovery periods of the Russell 2000 after a decline of 15% or greater since the index’s inception (12/31/1978).

So Even If There’s a Correction…

We do not see a significant decline or bear market for small-caps in the offing, though a correction in the 5-12% range would not be at all surprising to us and, in fact, would probably be healthy. With so many expecting a pullback, it would also be one of the most highly anticipated downdrafts in history.

Instead of a broad-based pullback, we think more rolling sector- and industry-based corrections are more likely in the months ahead, similar to what we saw for industrial stocks in 2015, healthcare in 2016, and energy so far in 2017.

…Value’s Leadership Looks Safe to Us

The current cycle has featured a pronounced leadership shift in favor of value, which owns a long-term performance edge over growth. This regime shift reversed a five-year run for small-cap growth (2011-2015).

We see this value-led cycle as a very healthy one, even with its ‘two steps forward, one step back’ pattern.

Since the inception of the Russell 2000 in 1979, prolonged periods of small-cap growth leadership have been both comparatively rare and succeeded by lengthy leadership stints for value.

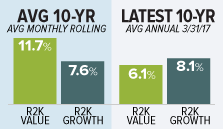

For example, over all monthly rolling 10-year periods, the average annual total return for the Russell 2000 Value was 11.7% versus 7.6% for the Russell 2000 Growth.

In contrast, for the period ended 3/31/17 the average annual 10-year total return for the small-cap value index was 6.1% versus 8.1% for its growth counterpart. The spread suggests to us that value’s leadership has a ways to go.

Outlook

2016’s Leadership Remains Intact

We see no rotations in long-term sector or style leadership and expect that the three reversals from 2016 that we’ve been emphasizing—positive long-term returns for small-cap, value leading growth, and cyclicals beating defensives—will remain in place, accompanied, we suspect, by higher levels of volatility.

The flat market from 12/9/16-3/31/17 may have been the small-cap pause that refreshes.

Here’s why: the economic news remains positive here in the U.S. and is improving globally; the small-cap earnings outlook remains decent to bright, depending on the industry; the dollar corrected slightly in 1Q17, which is a good sign for many small-cap companies; and, while rates are rising, yields have so far not elevated too quickly or too high.

Value stocks have also historically outpaced growth issues when the economy is expanding while also showing less sensitivity to rising rates than their growth counterparts.

So while we’re not expecting returns to move in a straight line up, we think it’s likely that small-caps have room to run.

Note: Article contributed to ValueWalk.com by The Royce Funds.

Category: Investing in Penny Stocks