Is Policy Skepticism Creating A Small Cap Opportunity?

Key Takeaways

Key Takeaways

- We believe small caps are becoming an increasingly attractive tactical opportunity amid policy skepticism in Washington, D.C.

- Loss of confidence in policymakers’ ability to achieve tax reform has created an opportunity in small caps, in our view, should a tax deal be reached in Washington, D.C.

- The potential for the U.S. dollar to reverse recent losses may also provide a boost to small cap performance.

- Risks include failure to reach a tax deal, the age of the business cycle, and elevated valuations.

We believe small caps are becoming an increasingly attractive tactical opportunity. The primary reason for our optimism is the amount of skepticism toward the Trump administration’s ability to move its policy agenda forward, particularly with regard to tax reform. Small cap stocks benefit disproportionately from a lower corporate tax rate because of their more domestic focus. We still think tax reform will be passed in early 2018 despite widespread skepticism, though likely a slimmer version than the Trump administration and congressional leaders have proposed. Here we discuss the opportunity in small cap stocks that may be developing as skepticism builds.

Policy Upside

Small caps have underperformed their large cap counterparts in 2017 but performance has been improving since the end of May. Year to date, the small cap Russell 2000’s 5.6% advance trails that of the large cap Russell 1000 (+10.5%), although small caps have outperformed large by 2% since the end of May. At a macro level, we believe one of the biggest reasons for the underperformance is the market’s skepticism toward policymakers’ ability to enact corporate tax reform and other pro-growth polices proposed by the Trump administration and congressional leaders. Unsuccessful attempts by Senate Republicans to repeal and replace the Affordable Care Act to date have no doubt added to the market’s pessimistic view.

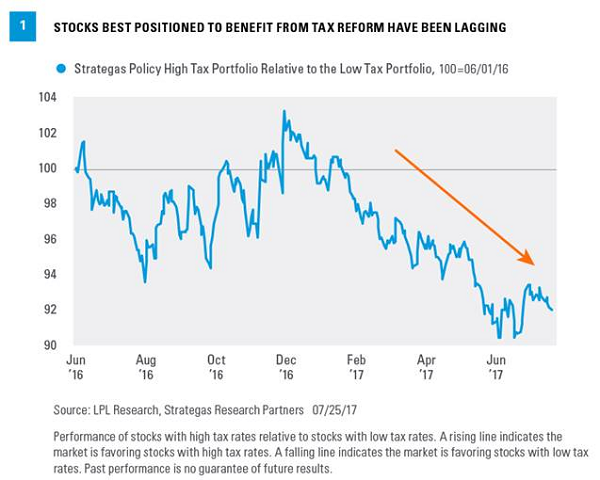

Figure 1 highlights this waning confidence in tax reform’s prospects. The chart represents the relative performance of stocks with high tax rates relative to stocks with low tax rates, from our friends at Strategas Research Partners. A rising line indicates the market is favoring stocks with high tax rates that are positioned to benefit most from a lower rate, while a falling line indicates the market is favoring stocks with low tax rates that benefit less from a lower rate.

Why do smaller companies like tax reform more? Simply put, smaller market cap companies generally have higher tax rates than their larger cap brethren—we estimate an average of about 5 percentage points higher—mostly because smaller companies generate a higher proportion of their earnings in the U.S. (earnings overseas pay lower tax rates). That means that smaller, more domestic-focused companies have more to gain from a potentially lower U.S. corporate tax rate, which we expect to make it through Congress and be signed by President Trump in early 2018—though it won’t be easy. Our optimism, though somewhat guarded, toward a potential tax deal suggests small caps may be poised to further close the performance gap with large caps in the coming months.

We should note that while we do expect a tax deal to get done, it may end up being a simple tax cut and not full reform. It is also important to keep in mind that a federal budget for 2018 must be finished first which won’t be easy and is probably the biggest impediment to any changes to tax laws at this point.

Currency Signals

We believe the potential for the U.S. dollar to reverse recent weakness is another reason that small caps are worth consideration as a tactical idea at this time. Given that geographic exposure is a key distinction between large and small cap companies, it is not surprising that foreign currencies tend to exhibit correlation with the relative performance of small caps versus large. We estimate that roughly 20–25% of small cap companies’ revenue comes from overseas markets, while the number for large caps is in the 35–40% range. Because of their more domestic focus, small cap stocks tend to (though not always) do better in strong U.S. dollar environments. A weak dollar helps multi-nationals more because they earn more revenue in foreign currencies that gets translated back into more dollars.

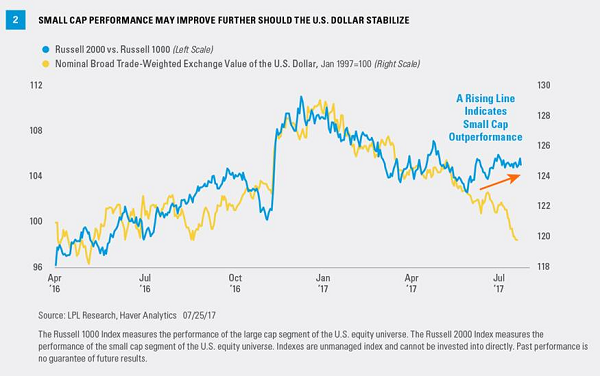

This relationship has been especially tight this year as shown in Figure 2, which charts the relative strength of small cap stocks versus large (blue line) against the trade-weighted U.S. Dollar Index (yellow line). Small caps and the dollar have moved closely together using this view, which covers the eight months leading up to the election in November 2016 and the eight months since.

This tight correlation is not particularly surprising given small caps and the U.S. dollar are both widely considered so-called “Trump trades.” Small cap performance has been and will likely continue to be dependent on prospects for tax reform. Foreign trade and other policies proposed and championed by the Trump administration tend to be positive for the U.S. dollar (even though the pro-U.S. dollar border adjustment tax is now off the table). More growth means more inflation, in theory, which tends to put upward pressure on interest rates, which in turn makes the U.S. dollar more attractive for foreign investors. Bottom line, the dollar is in some ways a barometer on the market’s confidence in the Trump administration’s ability to achieve its agenda.

Worth noting is that the two lines in Figure 2 have diverged some in recent weeks, with small cap performance improving while the dollar has weakened further. This divergence raises these questions: how fast will this relationship reconnect? And, how will it reconnect? Will small cap performance roll over or will the U.S. dollar begin to rally? Our bias is that a stronger dollar is likely to shoulder more of the load, rather than small caps rolling over, as the relationship is reestablished.

Risks

The biggest risks to consider with small caps in our view, beyond a tax deal not getting done are: 1) the age of the business cycle—small caps have historically not performed as well during the latter stages of an economic expansion, 2) should the broad market correct, small caps may potentially correct more given their greater economic and stock market sensitivity, and 3) valuations are on the high side, though we would argue that large cap valuations are also on the high side and therefore, on a relative basis we view small caps as fairly valued.

We should also point out that repatriation, which is likely to be part of any tax agreement, is more pro-large cap. Larger companies have more cash overseas and therefore benefit more from a lower (potentially very low) tax rate on overseas cash brought back into the U.S. Should the market grow increasingly optimistic that this policy will be enacted, though confidence is already high for this particular element of the tax equation, we would likely see increased investor enthusiasm for large cap companies with the most cash.

Bottom Line

We believe the policy pessimism still reflected in small cap stocks sets up a potential tactical opportunity. We are not in the typical sweet spot of the economic cycle and we certainly would not characterize small cap stocks as attractively valued. But should a tax deal in Washington, D.C. be reached, which we continue to believe is more likely than not, we would expect small caps to build on improved performance in recent weeks.

Note: This article was contributed to ValueWalk.com by LPL Financial.

Category: Investing in Penny Stocks