5 Deeply Undervalued Stocks With Great Dividends

Buy these five stocks today while their yields are high and their shares are cheap. With the rest of the market slightly overbought, purchasing these cheap dividend stocks with above-average yields will put you miles ahead of most investors who chase the hot stock of the minute.

Buy these five stocks today while their yields are high and their shares are cheap. With the rest of the market slightly overbought, purchasing these cheap dividend stocks with above-average yields will put you miles ahead of most investors who chase the hot stock of the minute.

Income investors might not have been as comfortable as usual for much of the last decade. Thanks to the Federal Reserve quintupling its balance sheet since the financial crisis as well as other extraordinary measures taken by the central bank, interest rates remain near historical lows, even seven years after the economic “recovery” began in June of 2009.

While this might be great for financing the massive and growing national debt as well for other debtors, it has been a huge albatross for savers and retirees. Traditional interest bearing vehicles like certificates of deposit pay practically nothing. This is forcing millions of savers out of their comfort zone and into the equity markets in their search for a decent yield.

This is a key reason traditional dividend sectors like Consumer Staples and Utilities are selling at stretched valuation levels based on historical averages. To me, these are two of the most dangerous areas of the current market to be invested in, although both sectors are usually thought of as “low beta” (low volatility) within equities.

Desperate income seekers are paying north of 20 times earnings for entities showing little in the way of earnings or revenue growth, and only to capture a three percent yield. I am avoiding both sectors completely within my own portfolio. When the day of reckoning comes, it will not be pretty for holders of these sectors.

I think income investors need to think outside of the box and explore other opportune areas to earn yield within the equity market. Here are the stocks that I invest in for dividends within my own portfolio.

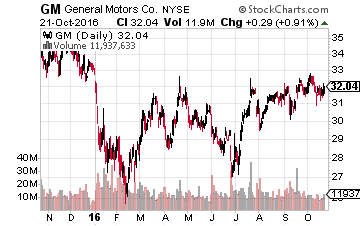

Let’s start with General Motors (NYSE: GM), which reports quarterly numbers early next week. I expect the American manufacturing icon to easily beat expectations. First, because the company has blown away the consensus bottom line estimate for five straight quarters. In addition, the consensus estimate has fallen from $1.52 a share three months ago to a current $1.44 a share. This is a bogey I expect General Motors to easily step over next week.

Let’s start with General Motors (NYSE: GM), which reports quarterly numbers early next week. I expect the American manufacturing icon to easily beat expectations. First, because the company has blown away the consensus bottom line estimate for five straight quarters. In addition, the consensus estimate has fallen from $1.52 a share three months ago to a current $1.44 a share. This is a bogey I expect General Motors to easily step over next week.

North American auto sales have likely plateaued after last year’s record levels. However, gas prices are likely to remain low given the glut in crude. This means the company’s overall sales mix will remain tilted to trucks and SUVs which have much, much higher profit margins than cars. Consumers are more inclined to purchase the roomy gas-guzzlers when the cost to fill up remains low.

Car sales in Europe look to be on the mend and after years of recession-level sales. This pent up demand should mean several years of slowly improving vehicle sales.

The most bullish news on the company, however is that they are killing it in China, the largest auto market in the world that seems to get overlooked. GM continues to take market share via joint ventures in the Middle Kingdom and is well positioned in this critical market for the future.

The company also continues to return cash to shareholders via stock buybacks and dividends. The shares currently yield 4.8% and sell for less than six times this year’s earnings. One of the best combinations of yield, growth, and value in the current market.

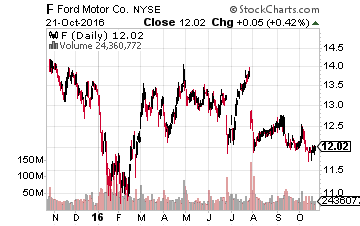

I also have a stake in competitor, Ford (NYSE: F), but only half the shares I hold in GM. General Motors is executing on its growth strategy better right now than its cross-town rival. However, selling at six times earnings with a five percent yield also makes Ford a good value in the current market.

I also have a stake in competitor, Ford (NYSE: F), but only half the shares I hold in GM. General Motors is executing on its growth strategy better right now than its cross-town rival. However, selling at six times earnings with a five percent yield also makes Ford a good value in the current market.

I also continue to like the lodging real estate investment trust sector for yield opportunities. This is especially true as many names are 25% to 35% off from 52-week highs as fundamentals have deteriorated slightly as the economy has averaged only one percent GDP growth over the past three quarters.

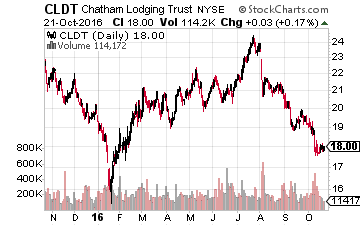

However, there are solid long-term values here. Chatham Lodging Trust (NASDAQ: CLDT) is one such name. I have owned the shares since they sold at $10 a piece in 2012. They now go for $18.00 a share even after their recent sell-off. Dividends have more than doubled over that time frame and this entity now yields over seven percent and makes payouts monthly. It has an extremely solid management team and sells for under eight times FFO (Funds from Operations).

However, there are solid long-term values here. Chatham Lodging Trust (NASDAQ: CLDT) is one such name. I have owned the shares since they sold at $10 a piece in 2012. They now go for $18.00 a share even after their recent sell-off. Dividends have more than doubled over that time frame and this entity now yields over seven percent and makes payouts monthly. It has an extremely solid management team and sells for under eight times FFO (Funds from Operations).

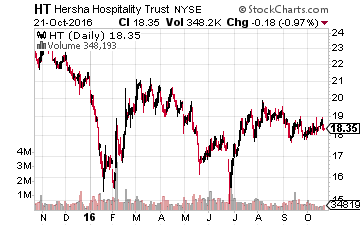

Hersha Hospitality Trust (NYSE: HT) is a lodging REIT that is a recent addition into my income portfolio. It is valued similarly to Chatham and has a yield of six percent. The REIT has also seen some insider buying of late as well which is always a good vote of confidence.

Hersha Hospitality Trust (NYSE: HT) is a lodging REIT that is a recent addition into my income portfolio. It is valued similarly to Chatham and has a yield of six percent. The REIT has also seen some insider buying of late as well which is always a good vote of confidence.

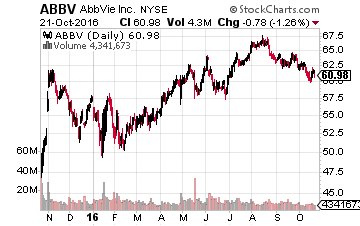

Finally, moving on to the beaten down biotech sector; one must like AbbVie (NYSE: ABBV) at current levels. The stock yields more (3.7%) than a lot of Utility stocks at current prices. It is also experiencing double-digit growth in earnings and revenue and goes for just over 12 times this year’s earnings per share. A more than solid combination of growth, income, and value.

Finally, moving on to the beaten down biotech sector; one must like AbbVie (NYSE: ABBV) at current levels. The stock yields more (3.7%) than a lot of Utility stocks at current prices. It is also experiencing double-digit growth in earnings and revenue and goes for just over 12 times this year’s earnings per share. A more than solid combination of growth, income, and value.

The low interest rate environment that has taken hold of the market for most of the last decade is likely to be with us for at least a few more years. Income investors should plan accordingly and target the right parts of the market for income at a more than reasonable price.

Top 5 Small Cap Biotech Stocks to Buy Today – The Names Might Surprise You

Bret Jensen thinks differently from most investors, and he is asking you too as well. In his 3 newest reports, he reveals his top 5 biotech stocks to buy now and reveals compelling research why these stocks are imminent buyout candidates and are about to hand their shareholders massive paydays. There’s still time left to invest and Bret is giving away the tickers for free. Just click the link below.

Click here for the names of his top 5 picks in the small cap biotech sector.

Positions: Long ABBV, CLDT, F, GM, HT

Category: Breaking News