4 Takeover Targets In The Market’s Hottest Sector

There has been a fast and furious resurgence in M&A in this sector with tens of billions of dollars of deals going down in just the last couple of months. With expectations that dealmaking will continue to increase, consider these four stocks as solid investments with the chance for huge returns if they are purchased by a larger player.

There has been a fast and furious resurgence in M&A in this sector with tens of billions of dollars of deals going down in just the last couple of months. With expectations that dealmaking will continue to increase, consider these four stocks as solid investments with the chance for huge returns if they are purchased by a larger player.

After a total dearth of activity in both new IPOs and M&A deals within the biotech space over the first five to six months of the year, both areas have perked up as of late. Several biotech companies have filed to go public recently including a near $175 million offering for the recently formed women’s health player, Myovant Sciences (Pending: MYOV) and an approximate $85 million public offering for rare disease company, Ra Pharmaceuticals. The former is aiming for a NYSE listing, while the latter is slated for the Nasdaq. The fact that activity is starting to come back to the IPO market points to the improved sentiment on the biotech sector overall the space emerges from the deepest and longest bear market since 2008.

After being down over 60% in the first half of 2016 compared to the same period a year ago by dollar volume, M&A activity has also begun to perk up. Pfizer (NYSE: PFE) has been particularly active, gobbling up over $20 billion worth of acquisitions in three separate transactions over the past three months. But who are the likely hunters and targets in the M&A space right now?

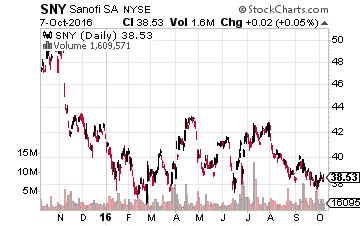

Let’s start with Sanofi (NYSE: SNY) which has been the “bridesmaid” a couple of times over the past year but never the bride. With money committed to making purchases as well as an urgent need to replenish its pipeline and product portfolio, the French drug giant is most assuredly on the prowl because its shareholders are becoming impatient with its stagnant growth.

Let’s start with Sanofi (NYSE: SNY) which has been the “bridesmaid” a couple of times over the past year but never the bride. With money committed to making purchases as well as an urgent need to replenish its pipeline and product portfolio, the French drug giant is most assuredly on the prowl because its shareholders are becoming impatient with its stagnant growth.

First Sanofi got outbid for hyperkalemia entrant ZS Pharma, which AstraZeneca (NYSE: AZN) won with a $2.7 billion bid in November of last year. Then, months after pursuingMedivation (NASDAQ: MDVN), the French drug maker was outbid by a cool $3 billion in late August by the aforementioned Pfizer.

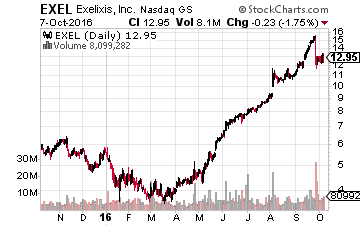

So where could Sanofi look next? Well, if we combine the focus on oncology with the target size of ZS Pharma, Exelixis (NASDAQ: EXEL) might make sense. The company has an approximate $3 billion market cap now and is one of the few true “mid-caps” in the biotech sector. Its primary compound CABOMETYX™ is one of the few new drugs I have seen recently that has easily exceeded initial sales projections. The drug was also just approved in Europe for certain types of kidney cancer and is in trials for other indications such as certain types of liver cancer. Biomarin Pharmaceuticals (NASDAQ: BMRN) is another mid-cap Sanofi and others have been linked to in the past but is a bigger fish with over a $15 billion market capitalization. This would be another one that could ignite a bidding war that Sanofi could easily lose.

So where could Sanofi look next? Well, if we combine the focus on oncology with the target size of ZS Pharma, Exelixis (NASDAQ: EXEL) might make sense. The company has an approximate $3 billion market cap now and is one of the few true “mid-caps” in the biotech sector. Its primary compound CABOMETYX™ is one of the few new drugs I have seen recently that has easily exceeded initial sales projections. The drug was also just approved in Europe for certain types of kidney cancer and is in trials for other indications such as certain types of liver cancer. Biomarin Pharmaceuticals (NASDAQ: BMRN) is another mid-cap Sanofi and others have been linked to in the past but is a bigger fish with over a $15 billion market capitalization. This would be another one that could ignite a bidding war that Sanofi could easily lose.

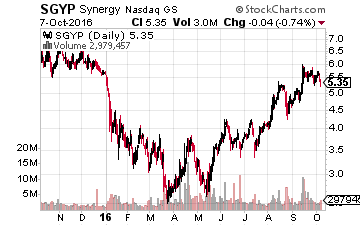

Allergan (NYSE: AGN) is another large drug maker that has plenty of “ammo” after selling its generic drug business to Teva Pharmaceuticals (NASDAQ: TEVA) for a cool $40 billion. The Irish concern has already made some small pickups and has stated it will continue to pursue “bolt on” acquisitions in four key treatment areas it desires to expand its footprint into. It has a key advantage via the low corporate tax rates in Ireland which allow it to bid higher for attractive takeover candidates including picking up small NASH concern Tobira Pharmaceuticals (NASDAQ: TBRA) for over a 600% premium recently – no that is not a typo

One of the areas Allergan is targeting is the gastrointestinal space. Synergy Pharmaceuticals (NASDAQ: SGYP) would make a lot of sense here given a just under $1 billion market capitalization. Its compound Plecanatide should deliver positive Phase III trial results sometime this quarter for the treatment of IBS-C. The compound also has a January 29th PDUFA date where that same drug should be approved for Chronic Idiopathic Constipation or CIC. Basically, the compound is a slightly faster acting version of Linzess with fewer side effects, notably diarrhea. Linzess does nearly $500 million in annual sales and appears to be headed to $1 billion in peak sales by 2020, absent new competition of course.

One of the areas Allergan is targeting is the gastrointestinal space. Synergy Pharmaceuticals (NASDAQ: SGYP) would make a lot of sense here given a just under $1 billion market capitalization. Its compound Plecanatide should deliver positive Phase III trial results sometime this quarter for the treatment of IBS-C. The compound also has a January 29th PDUFA date where that same drug should be approved for Chronic Idiopathic Constipation or CIC. Basically, the compound is a slightly faster acting version of Linzess with fewer side effects, notably diarrhea. Linzess does nearly $500 million in annual sales and appears to be headed to $1 billion in peak sales by 2020, absent new competition of course.

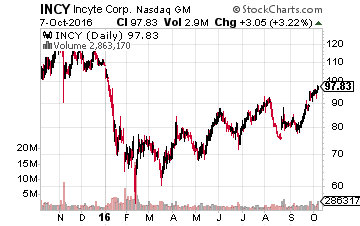

Merck (NYSE: MRK) has had declining sales growth for five years now thanks to key patent expirations. However, its oncology targeted Keytruda looks like it is on its way to blockbuster status. The company has a rock solid balance sheet and is finally looking like it will see some revenue growth over the coming year. I could see the drug giant being interested in a name like Incyte (NASDAQ: INCY) which has long been rumored as a buyout target. The companies are already working together assessing the combination of Incyte’s epacadostat and Keytruda in treatment-naive advanced/metastatic melanoma patients which is in mid-stage development.

Merck (NYSE: MRK) has had declining sales growth for five years now thanks to key patent expirations. However, its oncology targeted Keytruda looks like it is on its way to blockbuster status. The company has a rock solid balance sheet and is finally looking like it will see some revenue growth over the coming year. I could see the drug giant being interested in a name like Incyte (NASDAQ: INCY) which has long been rumored as a buyout target. The companies are already working together assessing the combination of Incyte’s epacadostat and Keytruda in treatment-naive advanced/metastatic melanoma patients which is in mid-stage development.

Incyte has a market capitalization of just over $17 billion and probably would cost upwards of $25 billion to purchase, but has an attractive drug pipeline and its oncology drug Jakafi is seeing solid revenue growth as well. Merck certainly has the balance to swing this sort of deal.

These are three ideas that could come to fruition should the “animal spirits” across M&A within the sector continue to perk up.

Finding biotech stocks with upcoming catalysts for explosive growth is a key component of my comprehensive strategy for massive profits in my newsletter, Biotech Gems.

Positions: Long AGN, EXEL, and SGYP

Category: Biotech Stocks