16 Under-The-Radar Stocks Quietly Yielding 10% To 36%

You won’t see these “hidden yields” quoted on any financial website. But these firms are showering their shareholders with double-digit yields – and making their owners rich in the process.

You won’t see these “hidden yields” quoted on any financial website. But these firms are showering their shareholders with double-digit yields – and making their owners rich in the process.

The key to finding them? Look beyond the stated yields and focus on the more nuanced (and more valuable) “shareholder yields”.

Take Corning (GLW) for example. The maker of Gorilla Glass never pays more than 3% – if you only look at the current dividend, that is:

Always a Modest 2%+ Yield

But Corning’s shareholder yield – which properly includes money the firm spends on share buybacks – has climbed into double-digits in recent years. Which is the main reason why shares have rewarded investors with 156% returns over the last five years:

Big Shareholder Yields, Big Returns

For example, over the last twelve months, investors received their 2% or so in dividends. But more importantly, they benefited from Corning repurchasing more than 16% of its outstanding shares in just one year.

Add the two up, and you’ve got an amazing 18% hidden yield. Again, you won’t see most of it reported anywhere – but over time, it will drive the share price higher.

Buybacks are underrated as a driver of returns. When the number of shares is reduced, every “per share” metric – dividends per share, earnings, and FCF – all improve. And their increases are leveraged to the amount of stock that is bought back.

After all, if profits are flat while float is reduced by 50%, the result is a 100% increase in earnings per share! And repurchases also support dividend growth. In Corning’s case, it has fewer and fewer shares to “settle up with” every year, so it can hike its payout more than it would otherwise with a static share count.

In a minute, I’ll share 16 stocks that:

- Have repurchased more than 10% of their shares over the past year,

- And yield 1.5% or better.

While the basket of them will probably beat the broader market, you and I can cherry pick the best of the lot by focusing on two rules.

Rule 1: Bargains are Better

Price matters when you and I buy stocks, and it’s no different for companies buying their own shares. If they overpay, they’re wasting money. But if their stock is a bargain, they’re making everyone money.

As recently as 2015, Corning was trading for less than ten times free cash flow (FCF). That’s a “no brainer” valuation, which makes management’s job pretty easy. It’s going to create more value buying back shares than dishing a dividend, in this case.

Check out the orange line below – Corning’s outstanding share count. Management put the pedal to the medal in 2014, when the stock was dirt-cheap. It’s recently started (smartly) to curtail buybacks now that GLW commands a higher valuation:

Smart Buybacks: Double Down When Shares are Cheap

This may be bullish for Corning’s next dividend hike (likely next February), but that’s a payout growth story for another day.

If bargains are good, then buybacks from great businesses are, well, great.

Rule 2: Growing Businesses are Best

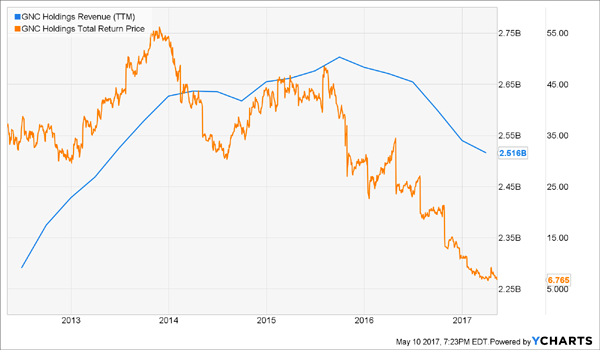

GNC Holdings (GNC) meets all the criteria we’ve discussed thus far. The company has repurchased more than 17% of its outstanding stock over the last year and paid and additional 11.8% in dividends.

It’s done everything right for shareholders, and the stock trades for just 10 times FCF today. Problem is, I’m not sure the company still has a business – its brick-and-mortar sales model is being eaten alive by the Internet.

GNC is trying to expand its offerings beyond its traditional “muscle head” base. The firm now sells nutritional supplements such as fish oil and supplements. And the number of transactions per store increased an impressive 9.3% last quarter.

But same store sales are mired in a downward spiral because the average transaction amount was down 12.1% at the same time! Company-wide sales topped out two years ago, and few stocks can thrive without top line growth. Even shareholder yield in the 30% range couldn’t help save this dinosaur:

When Sales Drop, the Stock Price Usually Follows

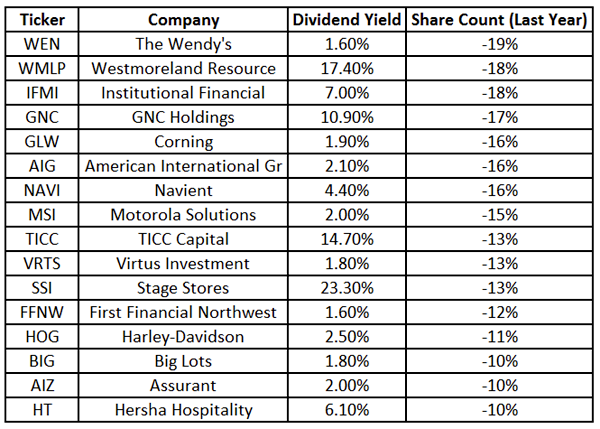

Stocks With 10%+ Buybacks & 1.5%+ Dividend Yields

The Retirement Portfolio You NEVER Have to Touch!

If you want to retire the way you’ve planned to for decades, you need the 8% across-the-board yields and strong growth potential of my “No Withdrawal” portfolio.

I’ve spent months researching high-yield stocks looking for the ultimate dividend plays that deliver everything we need to build a successful retirement portfolio. I had to weed out numerous value traps and yield traps, but the time was worth it because it resulted in this can’t-miss “No Withdrawal” retirement portfolio, featuring:

- No-doubt 6%, 7% even 8% yields – and in a couple of cases, double-digit dividends!

- The potential for 7% to 15% in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

These three critical elements will allow you to not only live off dividend income alone, but also grow your nest egg in retirement!

Let me show you the path to a no-worry retirement. Click here and I’ll provide you with THREE special reports that show you the path to building a “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential!

Category: Cheap Stocks